by Joshua Kaplan, CFA, Head of Research and Investment Strategy

Qualcomm announced on Monday that it had reached a deal with Apple to supply the world’s most valuable company with 5G chips for another three years. This unexpected announcement leads us to believe that Apple has been running into problems with the development of its own 5G chips whether they be technical issues or concerns around patent infringement. Regardless, the deal puts a spotlight back on the importance of 5G technology to the future of not only the communications industry, but the broader technology sector as a whole.

Let’s take a step back to gain perspective. The roll out of 5G networks in 2019 and 2020 brought the promise of a telecom capex cycle that was different from past generations. While previous upgrades provided a large but short-lived boost to earnings, the 5G cycle was expected to play out over many years with steadier growth for suppliers of the critical technologies that enable 5G networks to reach their transformative potential. Three years later we’re still in early innings of the 5G cycle.

5G technology’s power lies in three technological capabilities: enhanced mobile broadband (eMBB), massive machine-type communications (mMTC), and ultra-reliable low latency communications (URLLC). Each of these capabilities alone enhances the quality of mobile networks over 4G, but when used in conjunction they lay the technological foundation for some of the most promising technologies of the future including: industrial automation and robotics, autonomous driving, artificial intelligence at the edge, virtual/augmented reality and metaverse, and internet of things, to name just a few.

So why are we still in the early innings? Because the first phase of 5G rollout has focused mostly on eMBB (like most of the systems Qualcomm is supplying to Apple), which results in greater speed and capacity of mobile networks to meet growing demand in HD video streaming, mobile gaming, and mobile web browsing that were causing traffic jams in 4G networks. Moving on to mMTC and URLCC requires further investment in four enabling technologies: network densification, network slicing, network functions virtualization, and mobile edge cloud computing. This investment and roll out is expected provide demand for 5G technology and infrastructure companies for many years to come.

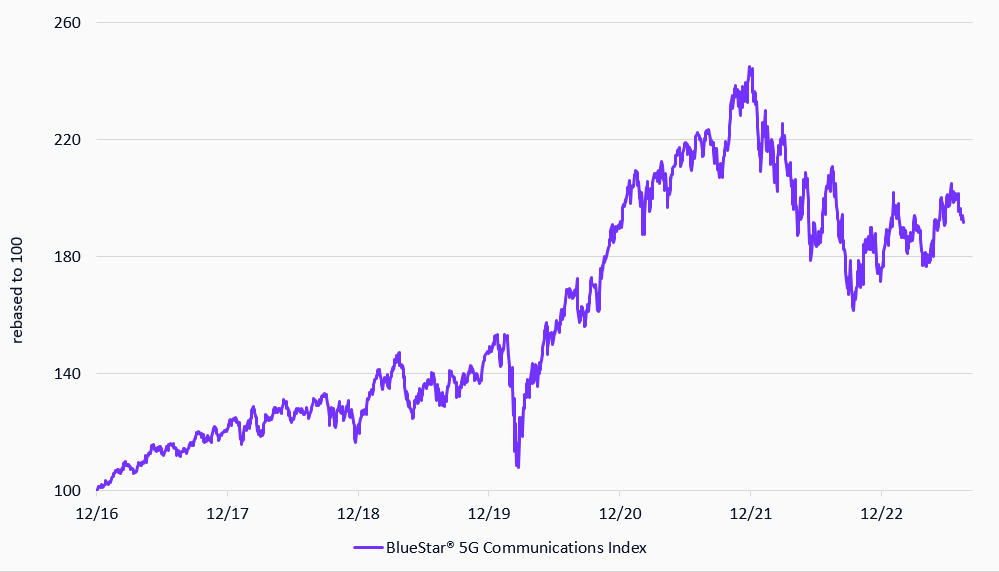

To capture the opportunity in 5G technology stocks, MarketVectorTM in 2019 launched the BlueStar® 5G Communications Index (BFIVG). With an update to the index’s methodology taking effect in September 2023, the index aims to capture the 50 largest and most liquid US-listed companies focused on providing solutions to support 5G infrastructure across all four of the enabling technologies and all three of the 5G capabilities mentioned above ranging from edge computing and software defined networking solutions to semiconductors solutions found in 5G cell tower equipment to cell tower/data center REITs.

While Artificial Intelligence has captured much of the spotlight in 2023 so far, 5G stocks continue to play a pivotal role in enabling such technologies of the future – taking artificial intelligence and machine learning at the network’s edge as a prime example – and Apple’s deal with Qualcomm serves as a reminder of the importance that 5G has in the broader technology landscape.

TOP-10 components as of Review Q3 2023

| APPLE INC | 5.00% |

| NVIDIA CORP | 5.00% |

| BROADCOM INC | 5.00% |

| CISCO SYSTEMS INC | 5.00% |

| ORACLE CORP | 4.82% |

| ADVANCED MICRO DEVICES | 4.21% |

| INTEL CORP | 3.82% |

| QUALCOMM INC | 3.38% |

| ANALOG DEVICES INC | 2.77% |

| ARISTA NETWORKS INC | 2.12% |

Source: MarketVector. Data as of September 8, 2023.

BlueStar® 5G Communications Index

12/31/2016-9/11/2023

Source: MarketVector. Data as of September 11, 2023.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryMarketVector Index(es) of the Month: Space

-

Commentary

CommentaryThe U.S. Regulatory Inflection Point