Cryptocurrency markets are still in their infancy and are susceptible to extreme volatility and bubble-like price patterns. Their prices tend not to follow efficient market behaviour which is generally assumed for developed markets. The price patterns of cryptocurrencies make a standard market value-weighted approach sub-optimal for indexation. Alternatively, dynamic, risk-optimised allocation schemes can generate superior returns on cryptocurrency markets over medium to long-term time horizons.

SEBAX vs. MVBTC since SEBAX Inception

| November 30, 2015 - February 14, 2020 | ||

|---|---|---|

| SEBAX | MVBTC | |

| Return (annualised) | 213.66% | 119.74% |

| Volatility (annualised) | 91.45% | 75.54% |

| Sharpe Ratio | 2.34 | 1.59 |

| Max Drawdown | -86% | -83% |

| VaR (1d,99%) | -13.61% | -11.51% |

| Conditional VaR(1d, 99%) | -18.76% | -13.69% |

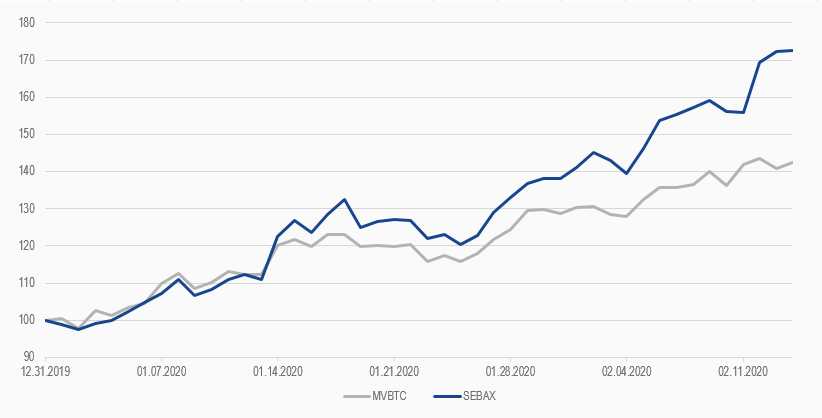

SEBAX vs. MVBTC YTD

| December 31, 2019 - February 14, 2020 | ||

|---|---|---|

| SEBAX | MVBTC | |

| Return | 72.56% | 41.98% |

| Volatility (annualised) | 57.30% | 45.16% |

| Sharpe Ratio | 1.27 | 0.93 |

| Max Drawdown | -9% | -6% |

| VaR (1d,99%) | -2.46% | -3.59% |

| Conditional VaR (1d,99%) | -3.92% | -8.55% |

Get the latest news & insights from MarketVector

Get the newsletterRelated:

About the Author:

Daniel Kuehne is Head of Asset Management at SEBA Bank AG. SEBA is a Swiss licensed bank and pioneer in the financial industry building the most comprehensive and secure bridge between digital and traditional assets (www.seba.swiss). He has long-standing experience in various senior positions in asset and wealth management and holds a PhD in quantitative finance.

SEBAX is a proprietary index of SEBA. Find further details on www.seba.swiss/seba-index.

The article above is an opinion of the author and does not necessarily reflect the opinion of MV Index Solutions or its affiliates.