In recent years, the lines between traditional finance and the world of crypto assets have become increasingly blurred. Strategies once confined to conventional markets, such as the Yen carry trade, are now making waves in the digital asset space, including Ethereum. As these financial worlds intersect, events in traditional markets can send shockwaves through the crypto landscape, leading to significant shifts. For investors, understanding these connections is key to navigating both markets effectively.

The Ripple Effect of the Yen Carry Trade on Ethereum

The Yen carry trade, a popular strategy involving borrowing in low-interest currencies like the Japanese Yen to invest in higher-yielding assets, has long been a cornerstone of traditional finance. However, when the trade unwinds—often due to sudden shifts in currency values or market conditions—it can trigger a domino effect across various asset classes, including crypto assets like Ethereum.

Recently, we witnessed this firsthand. As the Yen carry trade began to unwind, it led to a dramatic sell-off in multiple markets. Ethereum was not immune, experiencing a steep 26% decline. This sell-off was intensified by several factors, including a significant drop in Open Interest (OI) and massive liquidations of Ethereum by major players like Jump Trading. These cascading events not only shook the market but also created a surge in demand for Ethereum block space, leading to higher gas fees and unprecedented opportunities for Maximal Extractable Value (MEV).

Understanding Maximal Extractable Value (MEV)

MEV, or Maximal Extractable Value, refers to the extra profits that can be captured by validators when they decide the order of transactions in a block. Essentially, it’s the additional income they can earn by strategically arranging transactions to their advantage, especially during times of high market activity.

How the Unwind Boosted Ethereum Staking Rewards

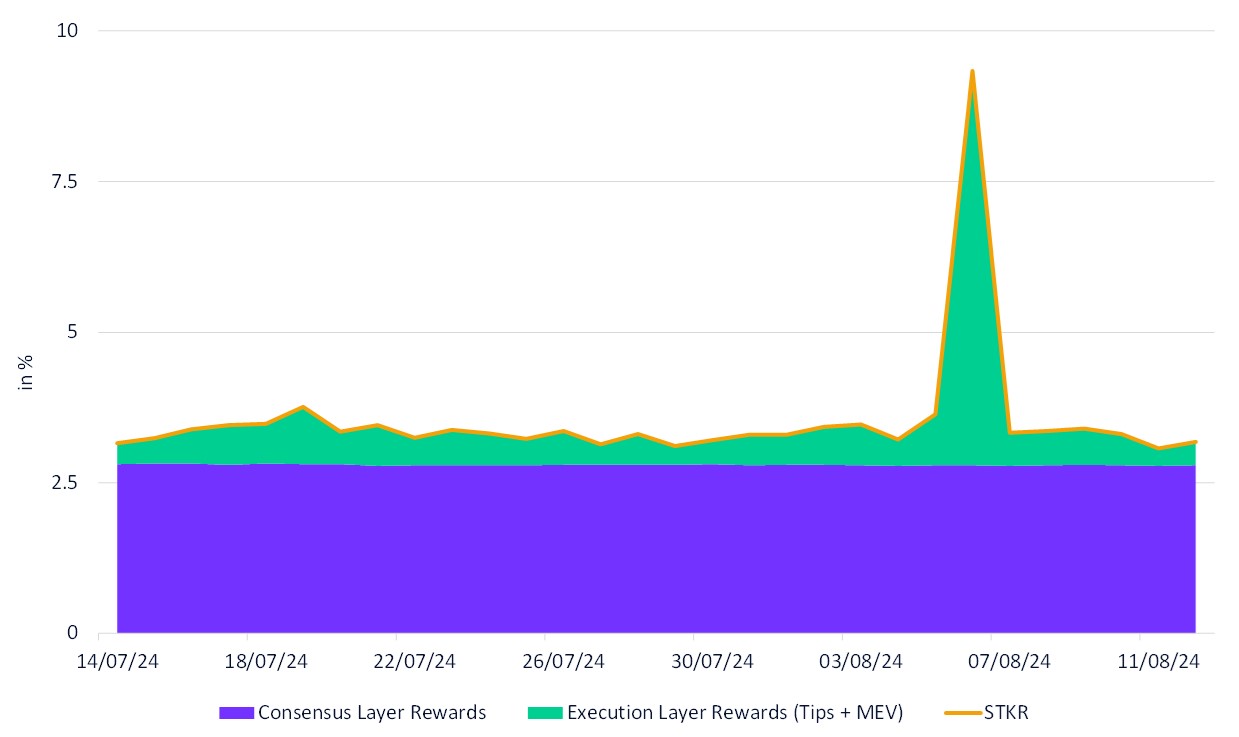

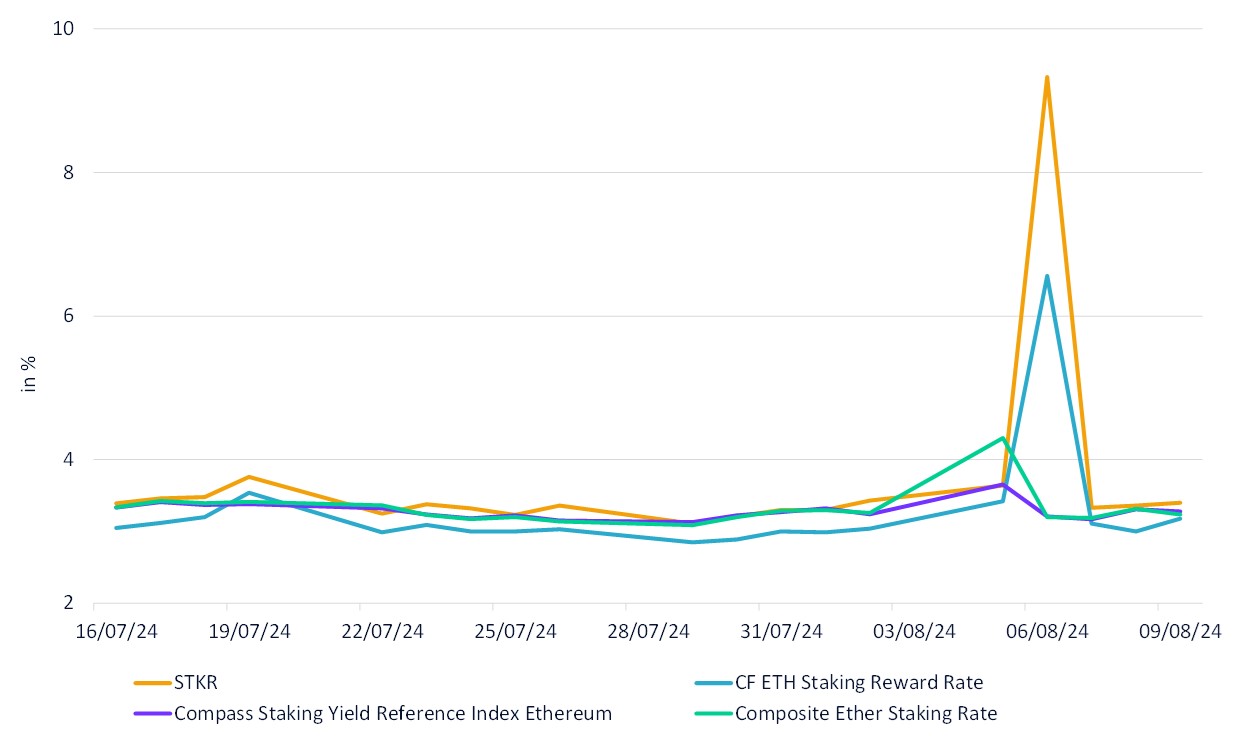

The chaos that followed the Yen carry trade unwind had a direct impact on Ethereum validators. As traders rushed to manage their positions, the spike in transaction volume on Ethereum led to higher gas fees and more lucrative MEV opportunities. Validators who could capture these opportunities saw their earnings soar, underscoring the importance of a comprehensive staking reward rate.

This is where the MarketVectorTM Figment Ethereum Staking Rewards Reference Rate (STKR) shines. The STKR Index includes not just the consensus layer rewards but also transaction tips and MEV of the whole Ethereum chain. This comprehensive approach provides a clearer picture of the actual rewards validators can earn, especially during times of market turbulence.

Source: MarketVector, Figment.

The STKR Index: Outperforming in Turbulent Times

During the recent market turmoil, the STKR Index stood out by offering a higher staking reward rate compared to other benchmarks. By factoring in all elements of validator earnings—consensus rewards, transaction tips, and MEV—the STKR Index provides a more accurate and reliable measure of staking rewards, particularly during volatile periods.

Source: Bloomberg,

For investors and validators looking to understand the full scope of their earning potential on Ethereum, the STKR Index offers a crucial advantage. It ensures that no aspect of potential earnings is overlooked, making it an invaluable tool in today’s rapidly evolving market.

Conclusion

The recent Yen carry trade unwind is a stark reminder of how interconnected global financial strategies and the crypto asset space have become. As these connections deepen, having a comprehensive and accurate measure of staking rewards is more important than ever. The STKR Index, with its holistic approach to calculating Ethereum staking rewards, has proven its value during these turbulent times, offering investors and validators a clear view of their true earning potential.

Read the Full Paper to explore how these financial shifts can enhance your staking rewards and how the MarketVectorTM Figment Ethereum Staking Reward Reference Rate (STKR) can guide your decisions.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

.png) Commentary

CommentaryAI Infrastructure