A Basket Approach To Digital Assets

June 2018

By Emre Camlilar, Product Manager, MV Index Solutions

"A Basket Approach to Digital Assets" download the PDF version

Digital assets—also known as cryptocurrencies—took the world by storm last year. While some associate digital assets with large price changes and volatility, others see them as the payment method of the future. This essay will focus on the growth and changes the digital asset market has experienced over the past year, and will discuss the potential advantages of investing in using a basket approach to invest in this new asset class.Table 1 shows the performance figures for a selection of the largest and most liquid digital assets, compared to the MVIS CryptoCompare Digital Assets 10 Index (MVDA10 Index)1, which uses a modified market-cap methodology to track the performance of digital assets.

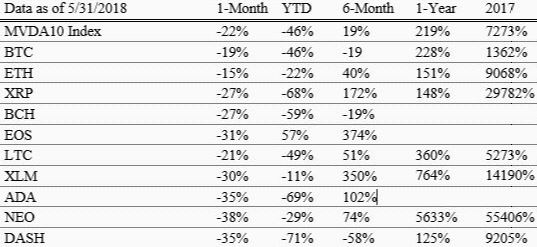

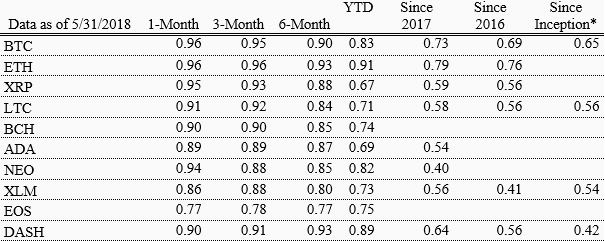

Table 1. Performance statistics in different time frames

Source: MVIS Research & CryptoCompare

At first glance, some digital assets such as NEO and Ripple (NEO & XRP) have experienced astonishing performance over the last year. An early 2017 investment in digital assets would have paid off, but the price boom of last year reversed in mid-January 2018. In comparison, the MVDA10 Index performed somewhere in the midrange throughout all time periods; it was neither the best-performing nor the worst-performing. This is in part thanks to its basket approach: By holding all of the above digital assets together, the MVDA10 index’s performance was smoother, and did not rise as high nor drop as low as many of its constituents.

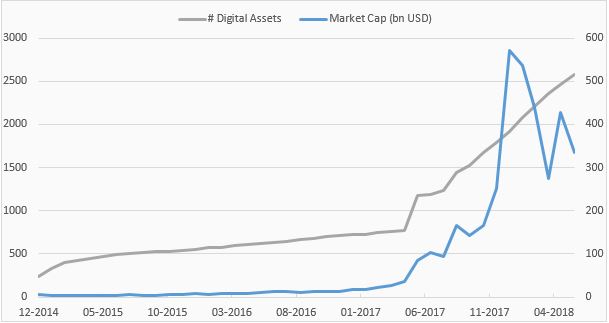

Although the performance for all digital assets has been negative year-to-date, it is clear that the amount of capital devoted to them has grown substantially since last year. Figure 1 shows that the total market capitalization in digital assets currently fluctuates between $300 billion and $400 billion—around 1.5 times less than when it reached its maximum level at the end of 2017, but still almost 300 times greater than its level at the beginning of 2017. Although the historical data might be too short, the current situation shows that there is a stable level of capital focused on digital assets.

Figure 1. Historical evolution of digital assets space

What does the size of the digital assets space tell us?

Although digital asset markets are extremely small compared with equity or bond markets, there is a growing interest in the market, and the sector may still be in its early stages. Digital assets and cryptocurrency have become topics of daily interest in the news media, while expertise in blockchain—the technology behind digital assets—has become the fastest-growing skill among jobseekers.2 This increasing interest can also be seen in the skyrocketing number of digital assets—depicted in Figure 1 above—which as of May 2018 had risen to 2577.3

Seen together as a whole, the rising amount of capital in digital assets, dramatic price movements, growing number of digital assets, news media attention and burgeoning job seeker interest all indicate the digital asset space is still in its early stages. Since their prices can be much more volatile than those of equities, it would be useful to take a closer look at a basket approach to diversifying digital asset investments.

How does a basket approach to digital assets affect volatility?

A basket approach aspires to limit downside risk through diversification. By spreading the investment over various digital assets, an investor can limit their exposure to single digital assets—which can experience more dramatic price swings—as well as lower volatility, which is an important consideration in such a volatile market.

To compare a basket approach to single digital assets, we will use the MVDA10 Index mentioned above as our “basket.” The MVDA10 Index tracks the performance of the 10 largest and most liquid digital assets by following specific and transparent rules defined by MV Index Solutions.4

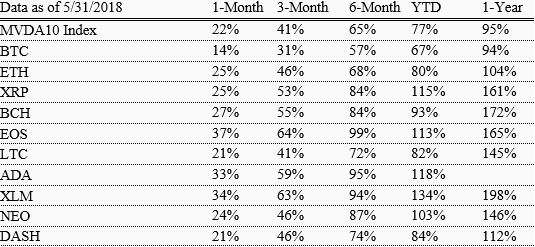

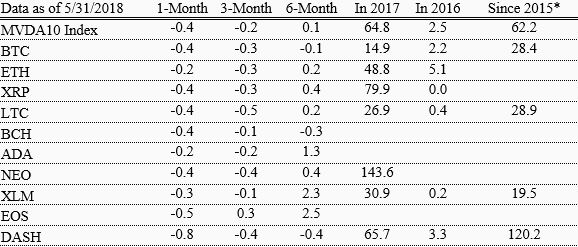

Table 2 shows the MVDA10 Index’s volatility statistics at the top, followed by those of the top 10 digital assets. When it comes to volatility, a lower number is better. Similar to the returns shown in Figure 1, the index’s volatility shown in Table 2 falls between the best and worst volatility statistics in all time ranges. Table 2 also shows that, when compared to the volatility of any single digital asset, MVDA10’s volatility tends to be lower. This is achieved through combining different securities whose price changes are not perfectly correlated to each other.

Table 3: Volatility statistics in different time frames

How does a basket approach correlate with digital assets?

One way to check whether two securities’ prices tend to move together is to use the correlation coefficient. The ratio itself does not provide any causal relationship for why two securities tend to move similarly, but it can measure the association between the price movements of two securities. The correlation coefficient falls between -1 and 1, where 1 implies a perfect positive relationship and -1 implies a perfect negative relationship between two given securities. As a very simple example, if one company produces only heaters while another produces only air conditioners, we can expect an almost perfectly negative relationship between these two. Note that the correlation of two securities changes over time, and can only be used to get an idea of the relationship between the price movements of two different securities within a given time frame.

Table 3 shows a comparison of correlation coefficients between the MVDA10 Index and the top 10 digital assets.

Table 3: Correlation between MVDA10 Index and digital assets

Source: MVIS Research, CryptoCompare

The correlation statistics above show an important trend. While the MVDA10 Index, which includes the top 10 digital assets by size and liquidity, has a correlation close to 1 with most of the digital assets in the short term, it consistently decreases over longer time periods. In other words, with a longer investment horizon, investors can benefit from diversification because the prices do not tend to move in parallel, meaning the individual risk of an asset has less of an impact over time. As a result, the volatility of the MVDA10 Index is lower than most of the single digital assets in all the time ranges. Now, let’s take a look at whether the return can be maximized at a given level of risk using the basket approach.

One measure for examining the risk-adjusted performance of risky assets is the Sharpe ratio. The Sharpe ratio gives a score to compare investments that vary in riskiness and return. It is generally accepted that a Sharpe ratio of 0.5 or higher is good, but it should be noted that this measure is a relative one, and is time-dependent; as such, it is only valid for a given time range.

Table 4: Sharpe ratios in different time frames

Bringing it all together: the benefits of a basket approach to digital assets

Digital assets have brought exciting new paradigms to both digital security and the concept of money. They have gained significant attention within the financial world, especially over the past year. Since digital assets can be so volatile, and their returns so divergent, investors may find a basket approach particularly well-suited to their needs.

As we showed above using the MVDA10 Index, a diversified basket approach to digital assets can provide decreased volatility and an average Sharpe ratio—potentially mitigating some downside losses that could be experienced when holding a single digital asset. Although a basket approach does not provide the very highest returns, its decreased volatility may be a welcome feature in such a volatile asset class.

2Please refer to the following link:

https://www.upwork.com/press/2018/05/01/q1-2018-skills-index/

3According to CryptoCompare

4Please refer to the following link for MVDA10 Index rules:

https://www.mvis-indices.com/index-guides

5 We will refer to the importance of pricing in digital asset markets in a separate essay.

Nothing in the commentary shall be considered a solicitation to buy or an offer to sell a security, or any other product or service, to any person in any jurisdiction where such offer, solicitation, purchase or sale would be unlawful under the laws of such jurisdiction. Please note that it is not possible to invest directly into an index. Neither MV Index Solutions GmbH nor any of its licensors makes any warranties or representations, express or implied, to the user with respect of any of the data contained herein. The data is provided for informational purposes only, and the Company shall not be responsible or liable for the accuracy, usefulness or availability of any information transmitted or made available through it.

Get the latest news & insights from MarketVector

Get the newsletterRelated:

Most popular

-

Commentary

CommentaryEthereum vs. Solana

-

Commentary

CommentaryGreat Expectations, Great Volatility