Russia's key structural problem is that the potential of its economic model based on rent-seeking and heavy reliance on the hydrocarbon exports is fully exhausted by now.

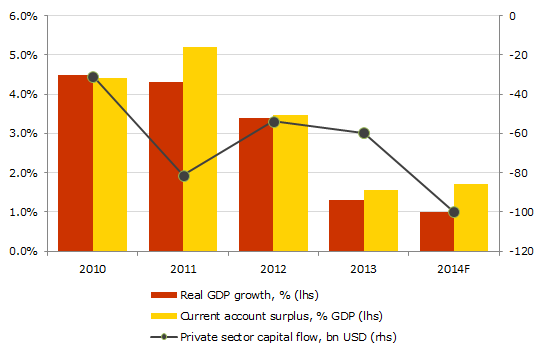

Despite high oil prices, Russia's current account surplus narrowed to mere 1.5% of GDP and real GDP rose only by 1.3% in 2013. Russia is also failing to address a major deterioration of its demographic situation which will weigh on growth and the public finances in the medium term. The standard policy shock-absorbents – the exchange rate and interest rate policies – are rigid with limited pass-through to the rest of the economy, whereas the public finances lack transparency.

Key immediate issues include large capital outflows and other balance of payments risks on the back of the Ukraine crisis/international sanctions and the need to rollover some 180 bn USD of the external debt maturing in the next 18 months (equivalent to approximately 40% of reserves).

Russia: Key Macroeconomic Indicators

Source: Bloomberg, CBR

Get the latest news & insights from MarketVector

Get the newsletterRelated:

About the Author:

Natalia Gurushina (PhD, Economic History, University of Oxford, 1995; BA, Economics, Moscow State University, 1989) serves as Chief Economist for emerging market managed debt strategies at VanEck. She has more than 15 years of industry experience including responsibilities at Roubini Global Economics, Pantera Capital and Deutsche Bank.

The article above is an opinion of the author and does not necessarily reflect the opinion of MV Index Solutions or its affiliates.

Most popular

-

Commentary

CommentaryGreat Expectations, Great Volatility

-

Commentary

CommentaryEthereum vs. Solana