By driving down the costs of financing, ultra-low interest rates have been supposed to deter savings and encourage borrowing, therefore stimulating the economy through increased consumption and investment.

It would appear, though, that in a number of countries with negative interest rate policies (NIRPs), for example, Denmark, Sweden, and Switzerland, exactly the opposite has happened.1)

As far back as April 2015, the Bank for International Settlements noted that, in such environments, “Ultra-low or negative interest rates will add to their [households’] worries by making it more difficult for them to build up enough retirement savings. Thus households are more likely to increase their savings rate then reduce it.” 2)

Even in the U.S. over the past several years there has been no evident trend of a decreasing saving rate. The question is, now: What can central banks do instead?

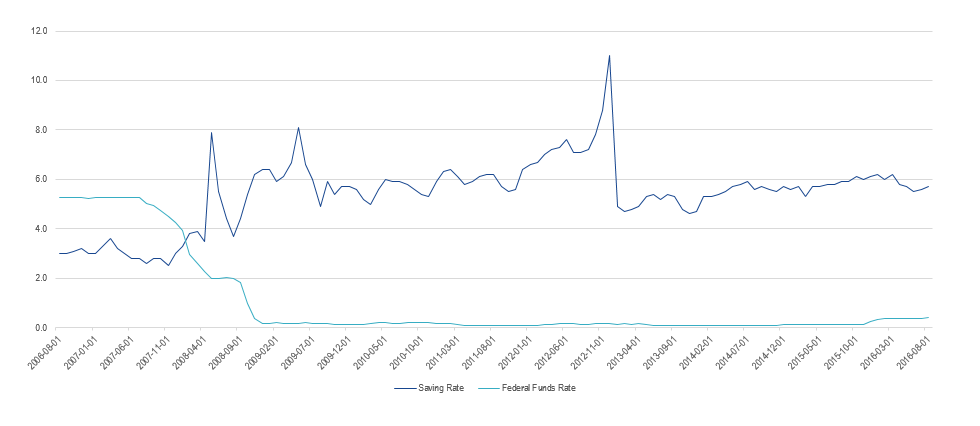

U.S. Personal Saving Rate3)

vs.

Effective Federal Fund Rate4)

Source: Federal Reserve Bank of St. Louis

Get the latest news & insights from MarketVector

Get the newsletterRelated:

About the Author:

William Sokol joined VanEck in 2016 as a product manager for VanEck Vectors ETFs, focusing on the firm’s international fixed income products. Prior to joining VanEck, Mr. Sokol held various product development roles at Prudential Financial, and was a derivatives structurer at BNP Paribas. Mr. Sokol holds a B.S. in Finance from New York University and is a CFA and CAIA charterholder.

The article above is an opinion of the author and does not necessarily reflect the opinion of MV Index Solutions or its affiliates.

Most popular

-

Commentary

CommentaryEthereum vs. Solana

-

Commentary

CommentaryGreat Expectations, Great Volatility